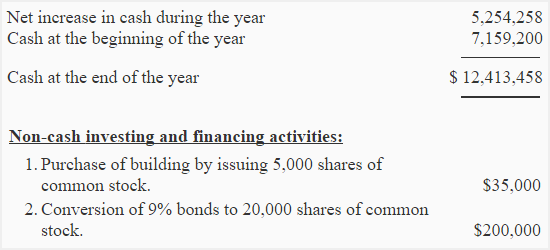

The general approach is to disclose a schedule of non-cash investing and financing activities at the bottom of the statement of cash flows. They can, however, also be included as a separate schedule or in the notes to the financial statements.

The general approach is to disclose a schedule of non-cash investing and financing activities at the bottom of the statement of cash flows. They can, however, also be included as a separate schedule or in the notes to the financial statements. In this presentation, we will take a look at the statement of cash flows non cash items. First question, why would we be looking at non cash items when considering a statement of cash flows?

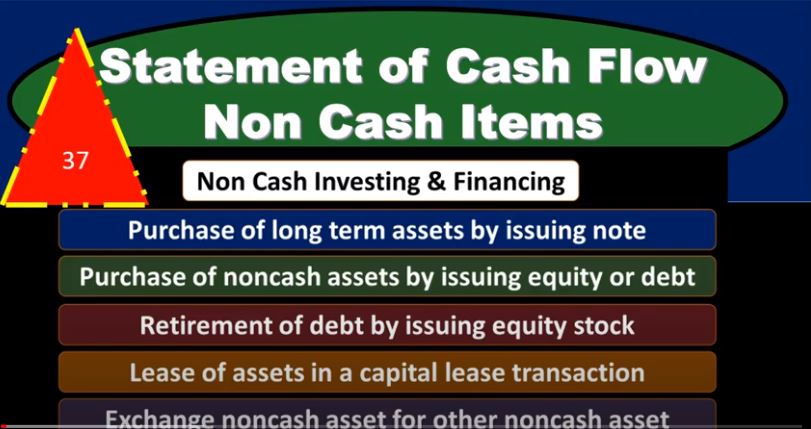

In this presentation, we will take a look at the statement of cash flows non cash items. First question, why would we be looking at non cash items when considering a statement of cash flows?/investing3-5bfc2b8e46e0fb0026016f32.jpg) In accounting, non-cash items appear on financial statements but do not impact cash flow. Examples of non-cash items include depreciation, amortization, and stock-based compensation.

In accounting, non-cash items appear on financial statements but do not impact cash flow. Examples of non-cash items include depreciation, amortization, and stock-based compensation.